Global Equity Divergence 2025: Why Some Markets Outperformed This Year?

Explore why China, Spain, Germany, and Italy led global stock market gains in 2025. Deep-dive into policy, sectoral shifts, valuations, and investor takeaways for better portfolio decisions.

Global equity markets showed dramatic divergence in performance over the past year, driven by unique combinations of macroeconomic shifts, government policies, sectoral strengths, and attractive valuations. Some regions posted outstanding gains while others remained subdued.

This article breaks down the reasons behind the outperformance of China, Spain, Germany, and Italy in 2025, transforming dense market insights into clear, concise paragraphs.

Global Stock Market Performance: 2024–2025

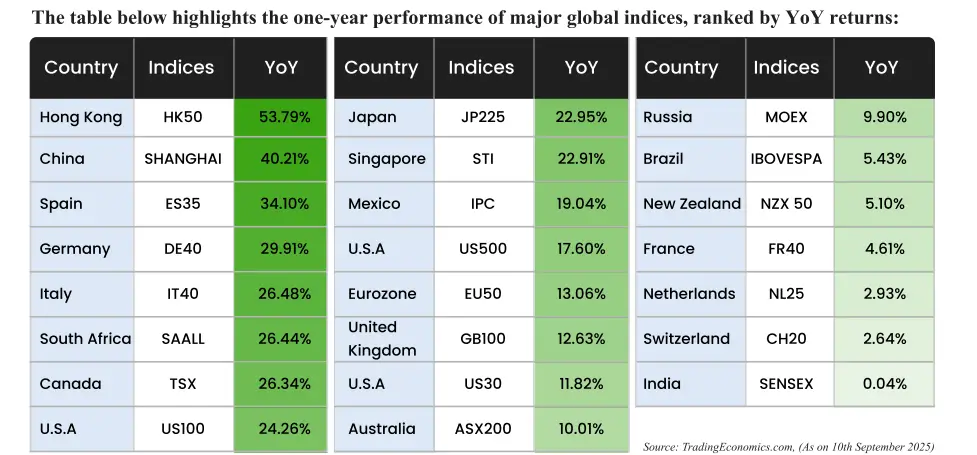

As of September 10, 2025, several indices stood out with exceptional returns. Hong Kong’s HK50 surged 53.79%, China’s Shanghai Composite advanced 40.21%, Spain’s ES35 gained 34.1%, and Germany’s DE40 posted gains of 29.91%. Italy’s FTSE MIB rose 26.48%, and South Africa, Canada, and Japan also performed strongly. In contrast, India’s SENSEX showed flat performance, highlighting the unevenness across regions.

China: Policy Power and Structural Shifts

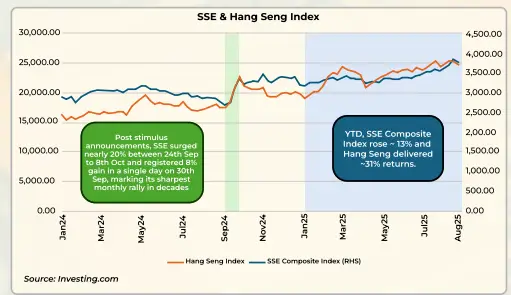

China led global outperformance with its Hang Seng Index and Shanghai Composite posting spectacular rallies. The robust momentum was primarily triggered by decisive policy support from Beijing in September 2024. The central bank pumped liquidity into the system through stimulus measures and easing in the property sector.

Both indices benefited from a surge in foreign investment as global hedge funds poured billions into Chinese equities. Investors were attracted by strong sectoral tailwinds. The Hang Seng Index rebounded due to its heavy exposure to technology giants, benefiting from eased regulatory pressure and renewed global enthusiasm for artificial intelligence and digital innovation.

Simultaneously, the Shanghai Composite received powerful support from China's shift towards new-economy sectors like electric vehicles, semiconductors, and clean energy. Electric vehicle sales soared to 11 million in 2024, with BYD leading at over 40% annual growth. By mid-2025, China’s solar capacity exceeded 1 terawatt, accounting for 67% of global solar expansion.

Low valuations also played a pivotal role. The Hang Seng traded at a P/E of 12.4, and the Shanghai Composite at 14.2, making them especially attractive for value-focused investors at a time when much of the world was seeking bargains.

Spain: Services-led Growth and Consumption Boost

Spain’s stock market delivered impressive gains, with the ES35 rising by 34% in a year. A critical driver was the country’s pivot towards high value-added services, which increased their share in GDP compared to pre-pandemic levels. This shift gave Spain a competitive advantage against other euro area economies.

Domestic demand remained resilient. Wages increased by about 4% annually, helping households maintain strong consumption despite macroeconomic challenges. The labor market stayed robust and inflation began to ease, creating a solid base for economic growth.

Immigration expanded the workforce and boosted consumption throughout the economy. On the market side, the IBEX 35’s composition – weighted toward banks, retail, and utilities – amplified these gains. Financial heavyweights like Santander, BBVA, and Caixa Bank outperformed as rising rates boosted net interest margins, while Inditex (owner of Zara) jumped 26% on surging retail demand.

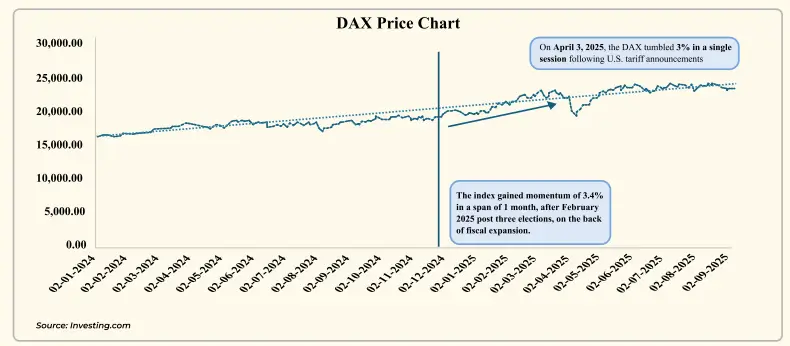

Germany: International Exposure and Fiscal Expansion

Germany’s DAX index reached new highs, recording nearly 30% YoY returns. Despite a sluggish domestic economy, German multinationals benefited from their significant global exposure. Only 20% of DAX companies’ revenues come from within Germany; the rest are spread across the eurozone, US, and China. A weaker euro further supported competitiveness abroad.

The February 2025 elections marked a turning point as the government launched a massive €500 billion infrastructure and defence program. This shift away from years of fiscal restraint reinvigorated market sentiment and drove a 3.4% gain in just one month.

Corporate standouts included SAP, which led the index on cloud growth strength, and Rheinmetall, which doubled on record defence orders. Siemens Energy delivered consecutive quarterly profits, while Allianz and Munich Re offered consistency through higher earnings. In contrast, German automakers lagged under pressure from Chinese electric vehicles and new US tariffs, causing disruptions in an otherwise strong year.

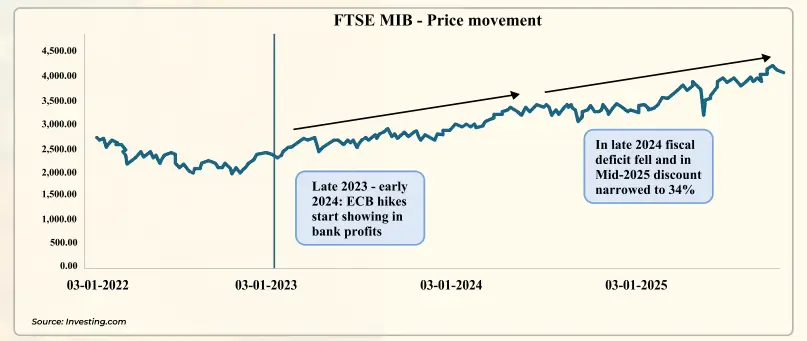

Italy: From Discount to Rebound

Italy’s FTSE MIB staged an impressive recovery, rising 26.5% after languishing at a 35-year low in 2023. The market previously traded at a 50% discount to global peers due to growth worries, political uncertainty, and a debt/GDP ratio above 130%. However, by mid-2025, the discount narrowed to 34% as improving fiscal discipline and stronger corporate earnings reignited investor optimism.

Banks led the comeback, capitalizing on wider net interest margins driven by ECB rate hikes since mid-2022. This ended years of low returns, resulting in record profits across the sector.

Selected corporates also stood out. Defence giant Leonardo soared more than 130% on booming NATO-driven demand, while Ferrari raced ahead with a 35% gain in 2024. Although Italy’s government revised growth forecasts down to 0.6% for 2025 and 0.8% for 2026, the fiscal deficit narrowed from 7.2% in 2023 to a projected 3.3% in 2025, approaching the EU’s stability threshold.

Lessons for Global Investors

This year’s market divergence underscores the importance of flexibility and global sector rotation. Aggressive policy interventions, fiscal stimulus, sectoral leadership, and attractive valuations proved decisive in determining winners. Markets trading at historical discounts, combined with structural economic shifts, attracted substantial capital and delivered outsized returns.

As always, investors should review all offer-related documents and consult financial advisors before making decisions. Past performance is not indicative of future results, and evaluating market risks remains crucial for portfolio construction.

Stay connected with Replete Equities for timely research and actionable insights.

Credit: This detailed analysis is based on an exclusive report by Centricity. We appreciate their efforts in creating this comprehensive global equity market overview.

Disclaimer: Investors are advised to read all offer-related documents carefully before making any investment decisions. Furthermore, indices data may vary due to differences in dates and reporting times Centricity Fincap Private Limited disclaims any responsibility for losses or damages arising from investments in debt securities, municipal debt securities, or securitized debt instruments, as these investments are subject to risks, including potential delays and/or defaults in payment. Users are encouraged to independently verify the accuracy and timeliness of this information prior to making any decisions based on it. Past performance is not indicative of future results, and market risks should be considered before investing. Kindly consult your financial advisor/consultant to verify the accuracy and recency of all the information prior to taking any investment decision.

Comments ()