India Market Outlook September 2025: Navigating Uncertainties with Strategic Insights

Discover expert insights on India’s economy, equity and debt markets, and investment strategies in the September 2025 Market Outlook. Explore how to navigate global challenges and domestic resilience.

India’s economic and market landscape in 2025 presents a dynamic picture marked by a mix of strong domestic fundamentals and significant external challenges. To help investors and market participants navigate this evolving environment, this article offers a detailed yet simple overview based on the comprehensive Market Outlook report by Centricity, shared via Replete Equities. It covers the key economic indicators, equity and debt market scenarios, commodity trends, and strategic investment ideas with a focus on actionable insights.

Economic Overview: Robust Growth Amid External Pressures

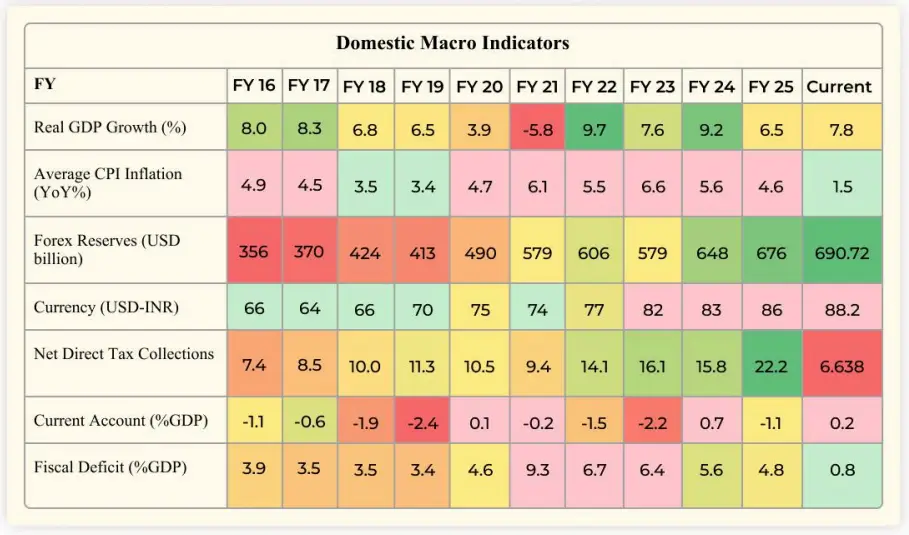

India began the fiscal year 2025-26 on a strong footing, with GDP growth reaching 7.8% in Q1, a significant improvement over 6.5% in the previous year. This rebound was primarily driven by sustained strength in services, government spending, construction, and manufacturing activity.

Despite this encouraging headline growth, a closer look reveals some subtle concerns. Nominal GDP growth – which better reflects actual income and spending in rupee terms – grew more modestly at 8.8%, down from 10.8% the previous quarter.

This divergence arises because inflation, which was historically higher, has dropped sharply to 1.5%, reducing the gap between real and nominal growth. A slowing nominal GDP can constrain tax revenue growth and impact corporate earnings, signaling cautious undertones beneath strong real growth numbers.

Inflation trends also provide important context. Having cooled to a six-year low in July 2025, inflation relief has allowed the Reserve Bank of India (RBI) to reduce the repo rate to 5.5%. The softer inflation supports domestic consumption and investment but introduces risks of inflation rebounding if global commodity prices or currency pressures intensify.

One notable macro development was the sovereign credit rating upgrade by S&P Global in August 2025, moving India’s long-term rating from BBB- to BBB—the first upgrade since 2007. This reflects improving fiscal discipline, sustained economic growth, and enhanced external stability. However, Moody’s and Fitch continue to maintain their previous ratings, underscoring the need for continued vigilance.

Despite the credit upgrade, India’s external position remains complex. The current account deficit (CAD) narrowed to just 0.2% of GDP in Q1 FY26, an improvement from 0.9% a year ago.

Yet, widening merchandise trade deficits due to tariffs and weaker export demand, coupled with moderating foreign direct investments and NRI deposits, have created underlying vulnerabilities.

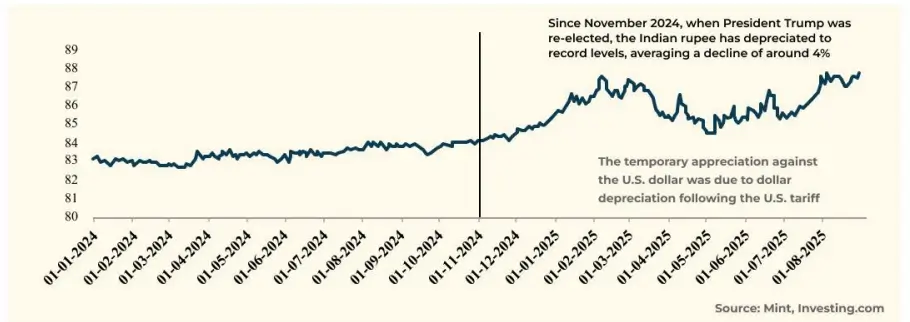

The Indian rupee depreciated more than 4% since late 2024, making it one of Asia’s weakest currencies and contributing to imported inflation risks.

Equity Market Outlook: Pockets of Strength Amid Valuation Caution

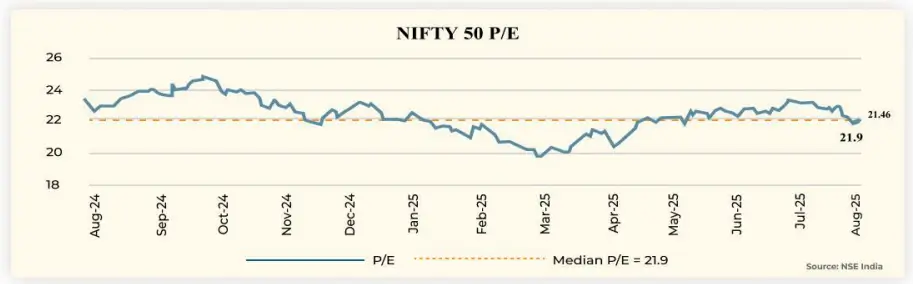

Indian equity markets have broadly held up during the ongoing period of global uncertainty, but the breadth of the rally remains narrow and concentrated in select sectors.

The Nifty 50 trades at a trailing price-to-earnings (P/E) ratio of 21.46x, marginally below its 10-year historical average but still elevated considering a slowdown in broad earnings growth.

Mid- and small-cap segments present even more stretched valuations, with Nifty Midcap 100 at 30.4x and Nifty Smallcap 100 trading around 31.5x P/E. This elevated valuation premium for smaller companies is not fully supported by earnings momentum and merits cautious, selective investing.

Sectoral performance has been uneven, shaped by global trade dynamics and domestic demand trends. Export-linked sectors such as textiles, chemicals, and allied manufacturing have come under pressure due to rising U.S. tariffs of up to 50%, leading to increased selling and muted outlooks.

The IT and pharmaceutical sectors, already challenged by softened earnings, continue to attract limited investor enthusiasm.

In contrast, consumer-facing fast-moving consumer goods (FMCG) companies buck the broad weakness with modest gains supported by steady domestic demand and anticipated benefits from GST rate cuts.

The automobile and metals sectors also displayed resilience, helped by robust domestic consumption and softening global dollar trends.

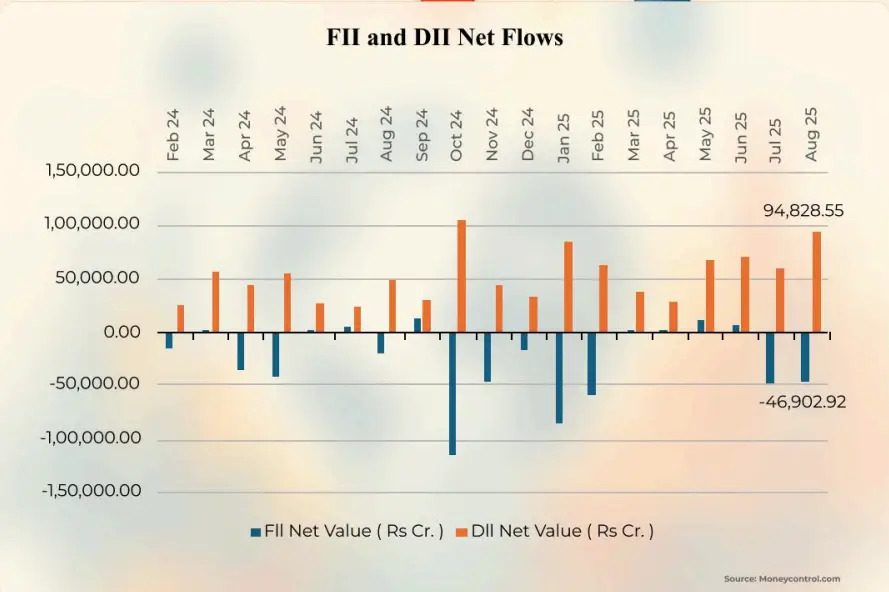

Institutional activity reflects this cautious market environment. Foreign Portfolio Investors (FPIs) witnessed heavy outflows, pulling nearly ₹47,000 crore from equities in August 2025.

The selling pressure is broadly attributed to the combination of tariff tensions, currency depreciation, stretched valuations, and rising U.S. bond yields.

On the other hand, Domestic Institutional Investors (DIIs) have sustained buying momentum, injecting over ₹94,000 crore in August, marking the 25th consecutive month of inflows.

Their investments have been concentrated in autos, consumer sectors, and private banks, demonstrating confidence in India’s underlying growth story despite near-term headwinds.

Debt Market Overview: Balancing Disinflation and Currency Concerns

India’s debt market reflects the interplay of favorable inflation trends and currency pressures. The 10-year government security (G-Sec) yield has eased from 6.86% in August 2024 to around 6.59% in August 2025, tracking the steady decline in inflation.

Short-term yields have responded to RBI’s accommodative stance, supported by cumulative repo rate cuts totaling 100 basis points in 2025. However, longer-term yields have remained sticky due to concerns about the rupee’s depreciation and the government’s substantial borrowing program.

The yield curve thus exhibits a modest steepening compared to the previous year, with longer maturities demanding a risk premium for currency and inflation uncertainties.

Globally, U.S. Treasury yields remain elevated on sustained inflation concerns and geopolitical risk premiums, while the European Central Bank has paused rate cuts amid sticky services inflation. These global factors influence India’s bond market sentiment, underscoring the need for cautious duration management.

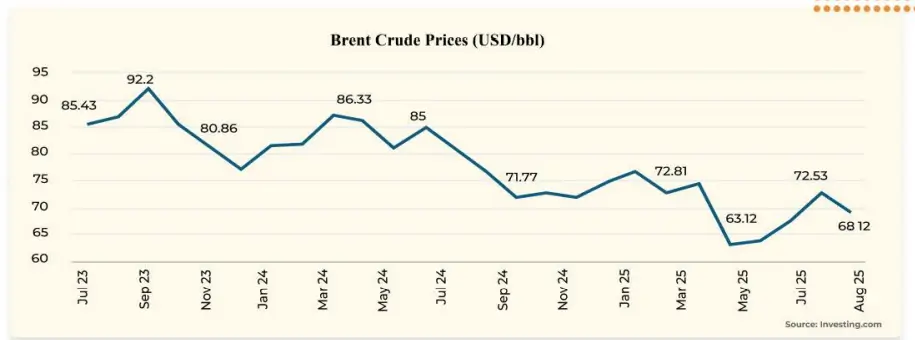

Commodity Market Outlook: Oversupply and Safe-Haven Demand

Brent crude oil prices continue to face downward pressure from increased supply and slowing demand, particularly in the U.S. OPEC+ has rolled back production cuts, adding over half a million barrels per day starting September 2025.

The International Energy Agency projects a surplus of up to 2.5 million barrels per day by year-end, which could drive prices below the mid-$60 range.

Precious metals remain a favored hedge amid persistent inflation and geopolitical tensions. Gold prices hovered around $3,429 per ounce in August, supported by central bank purchases and investor demand for safe assets.

Silver also gained strength, supported by rising demand from industrial sectors related to solar manufacturing and clean energy, along with its recent classification as a critical mineral by the U.S. government.

Investment Ideas: Balancing Growth and Risk

Given the intricate market environment—characterized by global shocks, domestic resilience, and valuation disparities—investors need a diversified and thoughtful investment approach.

Replete Equities, in collaboration with Centricity & Nuvama, recommends several investment strategies to balance growth potential with risk management:

- Flexible Equity Mutual Funds: The Motilal Oswal Business Cycle Fund offers the flexibility to navigate market phases by shifting across market caps, targeting a 14-17% expected return over three-plus years.

- Focused PMS Strategies: Portfolio Management Services focusing on mid- and small-cap special situations, technology themes, and emerging sector opportunities have delivered strong consistent returns, with 3-year CAGRs above 30%. Examples include Negen Capital’s special situation fund and Carnelian PMS led by seasoned market veterans.

- Debt and Credit Opportunities: Diversified multi-strategy credit funds such as Mosaic Multiyield Fund and Neo Special Credit Opportunities Fund target high single-digit to low double-digit IRRs with a focus on secured exposures, minimizing default risks.

- Absolute Return Funds: For investors prioritizing capital preservation and steady post-tax returns, absolute return funds offer lower volatility compared to broad market indices.

To position your portfolio optimally amid today’s complex market environment, consider leveraging the expert guidance and curated investment products offered by Replete Equities. Connect with us to explore personalized strategies that align with your financial goals and risk appetite. Contact us at [email protected] or call +91-7229945555 to begin your journey toward informed, balanced investing.

Disclaimer and Credits

The views expressed herein are for informational purposes and do not constitute investment advice. Past performance is not a guarantee of future results. All investment decisions should be made after consulting with qualified financial advisors and conducting personal due diligence.

This article is based on the detailed Market Outlook report prepared by Centricity Advisory Services Private Limited. Replete Equities publishes this simplified version to enhance understanding and accessibility for investors. Centricity assumes no liability for any losses arising from the use of this information.

Comments ()