Why Most Intermediate Traders Blow Up After Their First Profitable Phase

Learn why intermediate traders lose gains after early success and how structured risk management in options trading ensures long-term capital stability.

Many intermediate traders reach a phase where their performance improves significantly compared to their beginner stage, and for the first time, they experience consistent profits over a few weeks or months. This phase often brings a sense of validation, reinforcing the belief that their understanding of markets, price behavior, and option structures has matured enough to justify larger exposure and more aggressive capital deployment.

However, what frequently follows this profitable period is not sustained growth, but a sharp and sometimes devastating drawdown that wipes out a significant portion of accumulated gains.

This pattern is not accidental, nor is it purely psychological. In most cases, the root cause lies in the absence of structured risk management in options trading, especially at the portfolio level. While strategy selection and entry timing receive most of the trader’s attention, capital protection mechanisms often remain underdeveloped.

This article explores why intermediate traders tend to “blow up” after their first profitable phase and how disciplined risk architecture separates temporary success from long-term sustainability.

The First Profitable Phase: What Actually Changes

When traders transition from inconsistent performance to a stable profitable streak, several structural shifts begin to occur simultaneously, even if they are not consciously recognized.

First, execution improves. Traders become more selective with entries, avoid random setups, and apply technical or volatility-based filters more consistently. Second, emotional reactivity reduces compared to the beginner stage, which allows trades to play out with less impulsive interference.

However, alongside these improvements, another less visible shift begins to develop: gradual expansion of exposure.

During profitable months, traders often:

- Increase position sizes slightly after each successful cycle

- Add additional positions because “capital is working efficiently”

- Allocate more margin to similar strategy types

- Reduce hedging to improve net returns

These adjustments may appear rational in isolation. Yet collectively, they change the portfolio’s risk profile far more than most traders realize.

The early profitable phase rarely tests the strategy under extreme stress conditions such as sudden volatility spikes, macro-driven gap movements, or correlation breakdowns. As a result, the trader’s confidence grows faster than their risk framework matures.

This imbalance becomes dangerous.

The Confidence Trap: When Performance Alters Judgment

Success affects perception more profoundly than failure. While losses typically increase caution, profits often increase conviction.

Overestimating the Stability of an Edge

After several months of consistent returns, traders begin to internalize the belief that they have identified a stable edge in the market. They may conclude that their understanding of price action, implied volatility, or option spreads is now sufficiently advanced to justify larger capital deployment.

However, most trading edges are conditional. A short premium strategy may perform exceptionally well in declining volatility environments but struggle during sudden expansions. A breakout strategy may thrive in trending markets but underperform during prolonged consolidation.

Without understanding how their strategy behaves across different market regimes, traders mistake temporary alignment with market conditions for permanent skill.

When size increases before regime resilience is proven, drawdowns expand disproportionately.

Gradual Erosion of Risk Controls

The erosion of discipline rarely occurs in dramatic steps. Instead, it happens incrementally and often under the justification of “optimization.”

For example:

- Stop losses may be widened slightly to avoid being “prematurely stopped out.”

- Correlated positions may be taken across indices and stocks without recognizing cumulative exposure.

- Margin utilization may increase from conservative levels to aggressive deployment.

- Risk per trade may shift from 1–2% to 4–6% without formal recalibration.

Individually, these adjustments appear manageable. Collectively, they weaken the structural integrity of the portfolio.

This is precisely where structured risk management in options trading becomes essential, because options magnify exposure faster than linear instruments.

Why Options Accelerate the Damage

Options are nonlinear financial instruments, which means that risk does not increase proportionally with price movement. Instead, exposure shifts dynamically due to changes in delta, gamma, vega, and theta.

For intermediate traders who primarily focus on entry logic, this dynamic exposure shift often remains underappreciated.

For instance:

- A short option position can experience rapidly increasing delta as price approaches the strike due to gamma effects.

- A volatility spike can expand losses significantly for unhedged short premium traders due to vega exposure.

- Time decay assumptions can fail during directional acceleration, reducing the expected benefit of theta.

When position sizes are modest, these nonlinear effects remain contained. When size has expanded following profitable months, the same nonlinear dynamics produce accelerated drawdowns.

In other words, the blow-up is rarely caused by a new mistake. It is caused by the same strategy operating at a larger scale without enhanced risk controls.

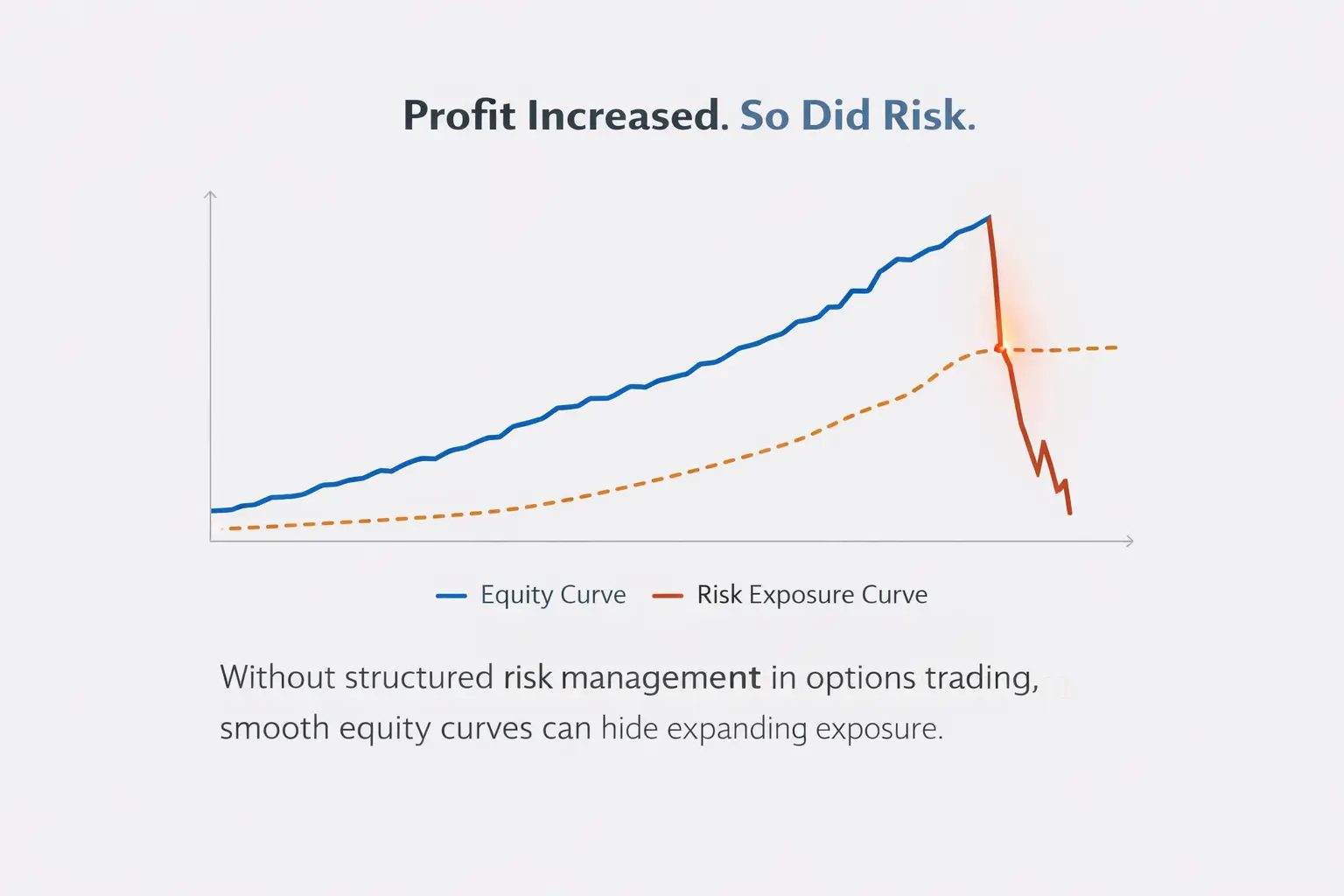

The Equity Curve Illusion

A smooth equity curve during profitable months creates a powerful psychological illusion of stability. Traders begin to interpret consistent upward movement as proof of robustness.

However, a rising equity curve does not automatically indicate controlled risk. In many cases, profits increase alongside expanding exposure, hidden leverage, or concentration in similar strategies.

For example:

- Selling options across multiple strikes may appear diversified but still concentrates vega risk.

- Running multiple short strangle positions across correlated indices increases systemic exposure.

- Allocating capital to similar expiry cycles creates time-based clustering risk.

When volatility conditions shift, these correlated exposures react simultaneously, leading to drawdowns that feel sudden but were structurally building beneath the surface.

Proper risk management in options trading requires analyzing not just trade-level risk, but aggregate portfolio exposure.

The Three Structural Mistakes That Trigger Blow-Ups

1. Absence of Portfolio-Level Risk Caps

Many intermediate traders define entry criteria but fail to define capital limits. Without explicit rules such as maximum daily loss, maximum weekly drawdown, or total margin caps, exposure can expand unchecked during profitable periods.

Professional frameworks always include predefined ceilings. These ceilings act as automatic stabilizers during stress events, preventing localized losses from escalating into structural damage.

2. Confusing Strategy Quality With Position Sizing Skill

A strategy with a positive expectancy can still fail if position sizing is inconsistent. Increasing lot sizes aggressively after wins introduces variability that may not align with statistical edge.

Intermediate traders often scale based on confidence rather than volatility-adjusted risk metrics. However, capital allocation should reflect:

- Historical drawdown tolerance

- Current volatility regime

- Correlation exposure

- Portfolio concentration

Sizing discipline determines survival more than entry precision.

3. Ignoring Market Regime Transitions

Markets do not remain static. They transition between low-volatility compression, expansion phases, directional trends, and event-driven dislocations.

Strategies that perform well in one environment may underperform in another. Without dynamic exposure adjustment, traders inadvertently carry inappropriate risk into changing conditions.

Effective risk management in options trading requires:

- Monitoring implied volatility percentiles

- Adjusting exposure before major macro events

- Reducing leverage during volatility expansion

- Rebalancing when correlations spike

Failure to adapt converts temporary edge into structural vulnerability.

What Professionals Do Differently

Professional traders operate with an explicit understanding that survival precedes profitability. Their primary objective is not maximizing short-term return but ensuring long-term capital continuity.

They implement:

- Defined risk per trade before execution

- Portfolio-level Greek monitoring

- Volatility-adjusted position sizing

- Structured drawdown response protocols

- Mandatory trading pauses after threshold losses

Importantly, they do not increase size solely because of a profitable streak. Scaling decisions are based on system robustness, not emotional reinforcement.

This disciplined approach transforms risk management in options trading from a defensive tool into a strategic foundation.

The Psychological Turning Point

The most dangerous thought in a trader’s development is the belief that the learning phase is complete. When traders assume they have mastered market behavior, they reduce documentation, neglect journaling, and loosen structural controls.

Confidence is necessary for execution. However, unchecked confidence erodes vigilance.

Long-term traders maintain structured humility through process adherence, regardless of recent performance.

Building Sustainable Risk Management in Options Trading

Intermediate traders who wish to transition into consistent performers must formalize risk architecture before scaling exposure further.

A sustainable framework includes:

- Clearly defined percentage risk per trade

- Portfolio-level margin caps

- Weekly exposure audits

- Predefined drawdown triggers

- Volatility-sensitive allocation models

- Mandatory size reduction during unstable conditions

Risk control must be proactive rather than reactive. It should function as a built-in system rather than an emotional response to losses.

When capital preservation becomes systematic, performance stabilizes.

Summary

Most intermediate traders experience significant drawdowns after their first profitable phase because they expand exposure faster than they strengthen risk architecture. Increased position sizes, correlated exposure, and underappreciated nonlinear risk in options create structural fragility beneath a smooth equity curve.

The issue is rarely strategy failure. It is usually inadequate risk management in options trading, especially at the portfolio level.

Early profitability builds confidence.

Long-term consistency requires controlled exposure, regime awareness, and disciplined capital allocation.

The traders who survive are not those who predict markets best, but those who manage risk most consistently.

A Structured Path Forward

If you are currently navigating a profitable phase, this is the appropriate time to reinforce structure rather than increase aggression. Developing institutional-style risk discipline early prevents structural setbacks later.

At Replete Equities, the focus remains on process-driven frameworks that prioritize capital protection, volatility awareness, and structured portfolio exposure.

To deepen your understanding:

- Explore the Option Strategies Mentorship Program for portfolio-level risk architecture

- Study the Intraday Option Selling Basket to understand exposure-managed execution

- Strengthen fundamentals through the Option Trading Foundations Program

Scaling should follow structure.

In options trading, disciplined risk management is not optional — it is foundational.

Comments ()